In an earlier article (“Is It Your Money?” which first appeared in the July 2015 issue), we used a sample remodeling project to explain how percent complete accounting works and why it provides a more accurate picture of job-related finances. In this follow-up article, we will deliver on our promise to “show how percent complete accounting helps flag a job that’s running off the rails.”

In our earlier article, the sample project assumed the job would progress exactly as estimated. This made it easy to show how the percent complete method results in a steady gross margin throughout the job compared with the misleading fluctuations of cash or accrual accounting methods.

But we all know that few jobs work out as planned. On the downside, some tasks take longer than we thought and end up costing more; on the upside, we may find savings through efficient ordering or by negotiating better terms with subtrades. Either way, while it’s difficult to know exactly how the job will end up, it is critical to be able to analyze costs during the project while there is still time to improve the final outcome.

In this article, we’ll look more closely at the same project—a $100,000 kitchen remodel with estimated costs of $75,000 and projected gross margin of 25 percent—beginning at six weeks in, the halfway point. By then, we should be able to determine whether or not the job is in trouble and, if it is, figure out where we can save some money.

Step 1: A Good Estimate

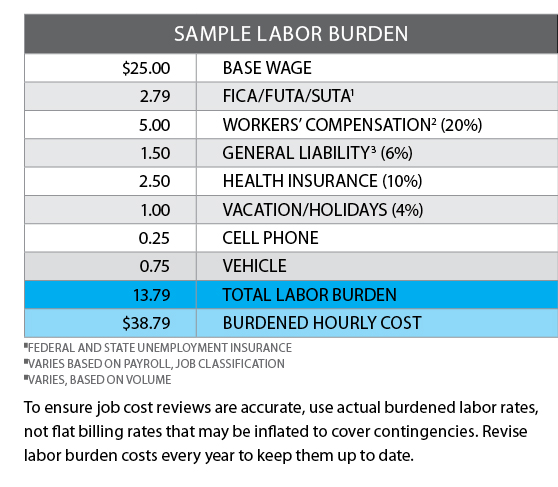

Because the percent complete method compares actual job progress to expected job progress, the original estimate must be as accurate as possible. The estimate for this kitchen includes all real costs, with no fluff added to individual line items. If you need to build in contingency money, do it as a separate line item. That will preserve the accuracy of your estimate-to-actual reports as the job progresses.

The labor rates used should reflect how much it actually costs to keep a field employee working on the job. They should not be “flat” billing rates artificially inflated to cover contingencies, but they should include all payroll taxes and other costs associated with maintaining employees.

In addition, larger dollar-value trade line items should be based on bids specific to this job for a clearly defined scope of work. Material estimates should use actual quotes or accurate historical numbers for lumber purchases and detailed specs for long-lead items such as doors and windows, tile, plumbing, and electrical fixtures.

Finally, specify as many products as possible to keep allowances to a minimum; this will reduce the number of adjustments you need to make as the job progresses.

Change orders must be estimated as well, both for hard costs and marked-up sales price, then used to adjust project cost. (Enter the change order estimate into your software as well.) Only then will the estimated amounts used in the job cost review include all possible costs and revenue.

Step 2: Effective Job Costing

Accurate actual costs depend on effective job costing. Production managers or lead carpenters must take responsibility for accurately coding vendor and trade invoices and for ensuring that timecards are up to date and error-free prior to data entry. As explained in the earlier article, costs are not entered when the invoice is received or paid, as is the case with accrual or cash accounting, respectively; costs must be entered in the reporting period in which the work was done (usually a month). This is relatively easy to do, except for the first few days of the following month, because most job-related costs posted then will be for work that was done during the previous month.

Step 3: Cost Analysis

To have any chance of achieving estimated gross margin, job costs should be analyzed frequently—at least after every payroll. The process brings sales and production together to review job progress and compare estimated and actual costs.

Print an estimate-to-actual report from your software and review each line item. Check the accuracy of costs currently in place

on the job as well as costs still to be incurred in future stages. Costs currently in place are easier, and your review should answer these questions:

- Are costs assigned to the right jobs?

- Are costs assigned to the right phase of work?

- Are costs assigned to the right cost type (labor, materials, trades, other)?

- Has the estimate been updated with all change orders?

The second component, future costs, is more difficult because the review involves some subjective judgments:

- Is the job on schedule?

- Are the trade bids equal to the estimated trade bids?

- Are material costs in line with the estimate?

- What is production’s “sense” of the job? Is it going well? Will it earn its target margin? Is anything out of whack with expectations?

These questions must be answered line item by line item. Looking at the bottom line won’t tell you where the job is making money and where it’s losing money. And it won’t tell you which trades or material vendors haven’t yet billed you for completed work.

Step 4: Dollars Left to Complete

This is the crucial step: calculating the dollars left to complete the project. The job cost estimate-to-actual report will give you the numbers you need to figure out where you’re ahead of the job and where you’re behind. Then you can plan how you will make up any slippage and where you may gain grippage going forward.

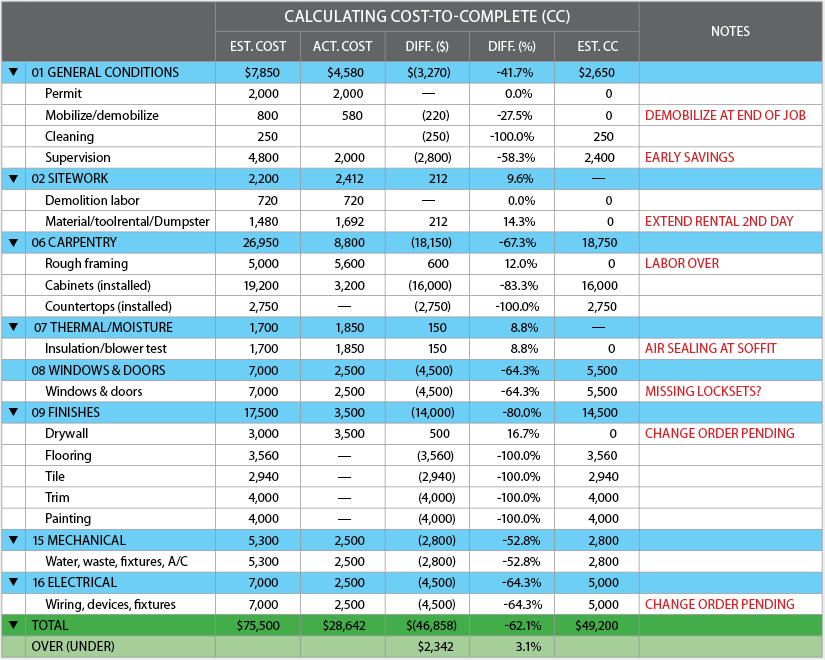

As an example, let’s look at the sample kitchen six weeks in—the halfway point (see “Calculating Cost-to-Complete,” on page 21). The project is already $2,342 over budget, with a lot of fussy work left to do. If savings can’t be found in the second half of the project, gross profit is at risk. Where will the savings come from?

A line-by-line review of the estimate-to-actual report shows the following:

01 General Conditions. Estimated cost for job supervision is ahead of schedule, but demobilization and professional cleaning need to come in on target because there isn’t much wiggle room.

02 Sitework. This work is complete with a slight overrun due to needing a rented chipping hammer and concrete saw for a second day. What caused that and how can it be avoided in the future?

06 Carpentry. Actual costs reflect a deposit with the cabinetmaker. Is the estimated cost to complete realistic given that the rough framing should be complete but isn’t? What’s the holdup?

07 Thermal Moisture. Was air sealing and fire blocking the soffit an estimating oversight or did the field crew drop the ball?

08 Windows & Doors. A couple of locksets are missing. Are they back-ordered or were they accidentally omitted? Could be more trouble brewing here.

09 Finishes. A drywall change order needs to be approved. (Undocumented and uncollected change orders are big drains on gross profit.) There may be room for some savings—is that tile on allowance?

15 & 16 Mechanical & Electrical. So far so good, assuming the change order is approved. Have all the finish fixtures on allowance been selected?

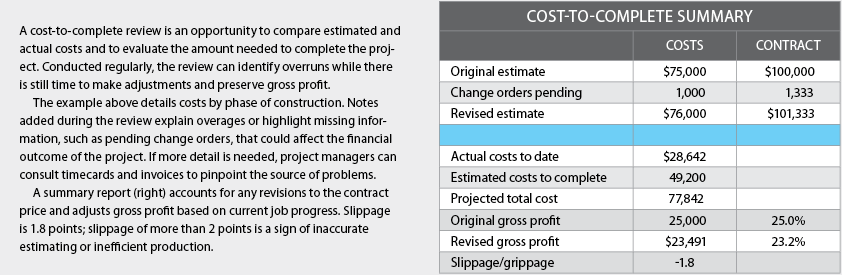

Looking at the “Cost-to-Complete Summary,” on page 21, the job is over-budget and gross profit slippage is –1.8 points (23.2% – 25%). This is not serious yet—a variation of more than 2 points reflects either inaccurate estimating or inefficient production—but it’s headed the wrong way. The fussy work is still to come, so there’s plenty of room to lose more. Fortunately, this analysis holds the information needed to find savings in the remaining phases of construction.

Ideally, you should do a cost-to-complete analysis earlier than this, when the job is 30 or 40 percent complete, and again at

about 80 percent complete—more often if you know things are

going south. PR

---

Judith Miller is a Seattle-based consultant to the remodeling industry and a facilitator with Remodelers Advantage specializing in accounting, financial management, and office systems.

Related Stories

Forty Under 40 Remodeling Trendsetters

The new ideas embraced by our Forty Under 40 winners are examples of forward-thinking leadership in remodeling

How to Create a World-Class Remodeling Team

Great remodeling companies position themselves for the future with the right players

How to Increase Your Odds of Closing Remodeling Sales

Use these tips to hone your sales process and grow close ratio

Everyone Should Have a Number: KPIs for Your Design Build Team

Measuring key performance indicators guides your team to success while creating accountability and ownership

Becoming Profitable in Your Remodeling Niche

The 2023 NAHB Remodelers Chair shares insights and advice for contractors in our 2024 Thought Leader predictions series

Combat Remodeling Market Pullback with Increased Marketing

Mosby Building Arts' president shares his expert predictions and approaches to remodeling in 2024 for Pro Remodeler's Thought Leader predictions series

A Mindset of Serving Others

A research study shows surprising results about what makes us take ownership of our work.

4 Surprising Home Improvement Trends for 2024

Leaf Home CEO Jon Bostock offers insight on topics and trends that will impact the home improvement industry this year