SageHome and the quiet collapse of a private-equity remodeling rollup

In recent months, the residential remodeling industry has seen a highly visible collapse: Renovo Home Services, a private-equity-backed rollup, filed for bankruptcy and abruptly shut down operations. But Renovo is not the only rollup to fail—and it may not be the most instructive.

Another PE-backed platform, SageHome, is now being unwound through a creditor-led foreclosure process rather than bankruptcy court. The failure has drawn little attention in the trade press, in part because it is happening quietly, through a mechanism many contractors may never have encountered.

Yet SageHome’s story offers a clear look at how rollups built during the COVID-era growth cycle can come apart once financing assumptions no longer hold.

SageHome set out to build a national remodeling company

Launched in 2022 as a private-equity-backed platform focused on aging-in-place bathroom remodeling, it targeted two categories that saw strong demand during the pandemic housing boom. In early press releases, they described “... a dual strategy of rapid organic growth and strategic acquisition to build its presence across the United States.” Cairngorm Capital Partners, a UK-based private equity firm active in the lower middle market, backed it.

The thesis was familiar: acquire strong regional operators, centralize systems and marketing, and scale quickly in a fragmented sector.

Between 2022 and late 2023, SageHome acquired at least five home improvement companies, including New Bath Today in Indiana; Midwest Bath Company in Illinois, Iowa, and South Dakota; CareFree Home Pros in Connecticut; Colorado Living in Colorado; and Safe Showers—later rebranded as BathWise—in Texas. In acquisition announcements during that period, SageHome reported that the combined platform had reached roughly $130 million in annual revenue and employed approximately 400 people.

By any industry measure, SageHome had achieved real scale in a short period of time.

Growth was financed—and then refinanced

Like many rollups formed during the pandemic-era expansion, SageHome relied on institutional debt to fund acquisitions and operations. Public disclosures show an initial secured financing in 2022, followed by a new financing agreement in late July 2024.

That refinancing appears to have marked a turning point. Rather than enabling another phase of growth, the 2024 facility coincided with a leadership change and was followed, within roughly a year, by creditor enforcement.

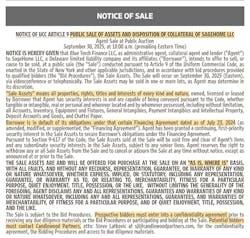

In early September 2025, Blue Torch Finance LLC, acting as administrative agent, initiated a UCC Article 9 public sale (see sidebar) covering substantially all SageHome assets, according to a legal notice published in The Wall Street Journal (page B4). The sale process is being coordinated by Candlewood Partners, a firm that specializes in lender-led asset dispositions.

SageHome did not file for bankruptcy. Instead, control of the company shifted directly to creditors.

SageHome’s assets are on sale

Under the UCC process, SageHome’s assets—including brands, intellectual property, contracts, and other operating assets—are being marketed for sale. Assets may be sold as a whole or in pieces, depending on buyer interest.

Pro Remodeler has contacted SageHome, Blue Torch Finance, Cairngorm Capital Partners, and Candlewood Partners to confirm details of the process and the scope of assets involved. SageHome CEO Joe Gorman replied that "...all brands are doing well and it is business as usual with our owner. There is no disruption to any sales, installation, or consumer activity."

What is clear from the public notice is that SageHome is no longer operating with a growth model. Its future—and the future of its operating companies—now seems to depend entirely on the outcome of the creditor-led sale.

This failure is different than Renovo’s

News of the SageHome unwind follows close on the heels of Renovo’s collapse, but the two cases differ in form. Renovo’s failure played out in bankruptcy court, with an abrupt shutdown that immediately disrupted jobs, employees, and customers.

SageHome’s failure is quieter. A UCC Article 9 sale happens outside bankruptcy, often with little public visibility—in fact, it happened months before the Renovo crash. From the outside, local operations may appear to be functioning—until ownership changes or assets are sold.

That quietness may make SageHome an instructive case. Rather than a sudden implosion, it reflects a slower unwind at the holding-company level after growth assumptions stopped aligning with financing realities.

Contractors and suppliers may be the last to know

SageHome’s failure was not caused by poor craftsmanship, weak local demand, or broken field operations. The stress emerged above the jobsite, at the corporate platform level, where debt service, refinancing risk, and capital structure matter more than production efficiency.

That distinction is critical for the industry.

When finance and operations are on different calendars, information doesn’t always flow concurrently. Subcontractors, installers, suppliers, and even acquired business leaders can find themselves exposed to corporate-level financial decisions they did not make. A creditor foreclosure is better than a bankruptcy, as Renovo did, but maintaining continuity between the company, customers, and employees after the sale is not guaranteed. Liabilities—such as warranties or customer deposits—are not always assumed by buyers, leaving homeowners vulnerable.

Just as important, SageHome shows how scale alone does not ensure resilience. At roughly $130 million in revenue, the platform was large enough to attract institutional capital—but still vulnerable to market fluctuations, like rising interest rates, cooling demand, and a generally herky-jerky market.

For smaller and mid-sized remodelers, the lesson is not about avoiding growth. It is about understanding how debt, refinance timing, and market assumptions can amplify risk—especially when growth is driven by leveraged acquisition rather than cash flow.

For larger firms and financial sponsors, SageHome is another data point in a growing pattern: rollups formed during the boom years now face a far less forgiving capital environment, where refinancing is harder, margins are tighter, and exits take longer.

A quieter pattern to watch

SageHome’s unwind did not come with a press release or a bankruptcy filing. It surfaced through a legal notice and a lender-run sale process that many in the industry may never notice. In fact, we were not looking for it when we stumbled upon it.

Once seen as the future of the fragmented remodeling industry, these rollup failures may become more common. Whether dramatic or quiet, shutdowns reshape companies, careers, local markets, and therefore, the industry.

Breaking down the pieces of a UCC Article 9 Sale

UCC: Uniform Commercial Code

Article 9: the section that broadly covers secured transactions in personal property (loans with collateral)

A UCC Article 9 sale is a creditor selling a borrower’s assets because they didn’t pay their debt

Instead of going to bankruptcy court, the lender (or an administrative agent acting on the lender’s behalf) can seize and sell the collateral securing the loan. That collateral can include brands, intellectual property, equipment, contracts, and other business assets.

Key characteristics:

- The sale is conducted outside the bankruptcy court.

- Assets are typically sold “as is, where is,” with no warranties.

- Buyers may acquire assets without assuming existing liabilities, unless they agree to do so.

- Continuity of operations is not guaranteed.

Because Article 9 sales are legal foreclosures rather than court cases, they often receive little public attention—even when large businesses are involved.

About the Author

Daniel Morrison

Editorial Director

Daniel Morrison is the editorial director of ProTradeCraft, Professional Remodeler, and Construction Pro Academy.