The Fall of a Remodeling Platform: Unpacking the Renovo Home Partners Failure

When Renovo Home Partners collapsed in late October, it wasn’t a single company that failed. It was a national platform built from some of the most recognizable names in regional remodeling—Reborn Cabinets, Dreamstyle Remodeling, NEWPRO Home Solutions, and Minnesota Rusco—that shut down almost simultaneously, leaving thousands of unfinished projects, unpaid employees, and stunned local markets in its wake.

For many owners and operators watching from the outside, the shock wasn’t just the speed of the collapse. It was who collapsed. “The business leaders of those businesses were some of the smartest people I know in the industry...” remarked Brian Gottlieb, an industry legend and author of Beyond the Hammer. They were profitable, long-standing local companies—some with histories stretching back decades—that had been sold into what was pitched as a sophisticated, well-funded national platform.

Former Reborn Cabinets CEO Vince Nardo learned of the shutdown the same way most of his employees and customers did. “I learned the same morning as everyone else,” Nardo said. Within hours, offices were closing, appointments were canceled, and workers were told to clear out. Paychecks stopped. Health insurance coverage vanished. Customers who had already paid deposits—or in some cases, the full contract price—were left with half-finished kitchens, torn-out bathrooms, and no clear path forward. “It’s just bad for the employees, the customers, the vendors—I don’t understand how it came to this,” Nardo said.

A home improvement CEO we spoke with, but who didn’t want to be named, described the failure as entirely self-inflicted. “The failure of Renovo has nothing to do with the marketplace,” he said, “It has everything to do with the equity firm and how they managed it from the very beginning.” The company still had value, and in fact, was in discussions the day before the shutdown about a possible spinoff. However, BlackRock, which held the senior debt, chose not to pursue a restructuring.

The scale of the fallout sent ripples far beyond the companies directly involved. “It sent a pretty big ripple out in the industry, for sure,” said Bill Owens, vice chairman of the National Association of Home Builders (NAHB), in an interview with Pro Remodeler. But from his vantage point, it is not evidence that the remodeling sector itself is unstable. Owens describes current conditions as a comedown from the extremes, not a collapse. The steep growth of the COVID-era home improvement market that fueled the overpriced sales of these companies has settled back to “normal,” even if 2025 was herky-jerky.

What followed was a scramble: homeowners calling attorneys general, lenders reversing funded loans, vendors freezing shipments, and competitors fielding calls from desperate customers. But beneath the chaos was a deeper question many in the industry began asking quietly—and then out loud: Are collapses like this inevitable? With the recent foreclosure and public sale notice of SageHome by creditors, many are asking that question louder. What looked to be the future of the remodeling industry just a few years ago doesn’t look quite so rosy anymore.

The structure couldn’t breathe

To understand what happened at Renovo, it helps to separate the businesses Renovo acquired from the structure into which those businesses were placed. By all accounts, the individual companies were operationally sound—generally debt-free cash machines. The platform they were assembled into was anything but. “Private equity plays a one-quarter game,” said Mark Richardson in an earlier column for Pro Remodeler, “remodeling plays a four-quarter game.” Richardson, who has advised many of the companies Renovo acquired, sees the failure as a story of incompatibility. Remodeling firms, he argues, are not designed like professional services firms or tech companies. They evolve slowly, shaped by local markets, founder intuition, and long cycles of hiring and training. The private equity finance people thought they were buying cookie-cutter widgets, but they were buying organisms. Gottlieb said it bluntly: “This was an example of a smart private equity group looking at [the industry] like stupid farmers. And if these stupid farmers could do this, imagine what smart private equity people could do.”

As long as pandemic-era demand was roaring and money was cheap, the math appeared workable. When growth normalized and interest rates rose, the structure lost its margin for error. By 2023 and 2024, refinancing events and debt restructurings became frequent. “What initially looked promising, with a strong demand for remodeling, became problematic as the work slowed to a more realistic pace—the debt service alone crushed the business,” said L. Burke Files, a former investment banker, fund manager, and author of Due Diligence for the Financial Professional. The platform’s total debt obligations ballooned, while operating cash flow failed to keep pace (chart, above). Beyond the crushing debt was a fundamental misunderstanding of the business that it owned.

Gottlieb adds, “I think they were making a knee-jerk reaction, based on what might have been a challenging month, with the first thought being, ‘How do we cut people? How do we slice marketing dollars? Instead of listening to the business leaders. If you want to summarize the failure, it was the shepherd not smelling like the sheep and not listening to the shepherds that do.” the CEO said much the same thing, “They lost so much of the culture that had been built. The speed of the leader is the speed of the business, and they lost the leaders.”

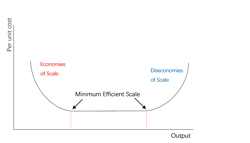

As pressure mounted, the response followed a familiar private-equity playbook: tighter reporting, aggressive cost controls, and leadership changes. Founder-CEOs who had built their businesses over decades were replaced or sidelined. Local autonomy eroded. Culture thinned. The economy-of-scale philosophy behind a rollup of similar companies sounds simple, but it comes with problems. Economists talk about the “diseconomy of scale” which occurs when the average cost per unit or per service increases as a company grows. It is tied to more compliance, worse communication, a bigger bureaucracy, and reduced employee motivation.

More isn't always better. Many are familiar with economies of scale, where a handful of individual operations can share services—like payroll, HR, marketing, and CRM—therefore saving money and increasing efficiency without losing services. Diseconomies of scale occur when too many organizations must share the same resources. The result is an increase in the cost per unit/service due to top-heavy bureaucracy and systems meant to work for everyone, which work well for no one. These can lead to demotivated workers short-cutting the system.

Burke explains it this way: “The three main issues I have seen [with diseconomies of scale] are management’s inability to coordinate large workforces, and the complex rules they create to ‘improve’ things only end up frustrating the workers. There’s also poor communication about what’s needed and where it’s needed. Companies used to have the parts nearby, but now they are centralized elsewhere to achieve economies of scale. The bureaucratic, slow decision-making and actions also lead to demotivation.”

It hit real people—and remodelers responded

With around 2,500 people suddenly out of work and roughly double that number of houses in various stages of disrepair, there was a national fallout. Inside that fallout were heartbreaking individual stories. One former employee who emailed Pro Remodeler was the “first point of contact with the customer,” and felt personally responsible for her community members who were affected. While she worried about potential homelessness, she felt personal responsibility for Renovo’s failure to run a business.

Vince Nardo also shared a couple of employee stories that, while extreme, illustrate very real human consequences. “We’ve had one confirmed instance of attempted suicide... and their daughter, a seven-year-old kid, found him—and he didn’t die.” Also, an employee who was let go in 2025 (before the collapse) was promised her health insurance would continue through 2026 because she was going through chemotherapy and cancer treatments. “They canceled her insurance at the end of the month,” Nardo reported.

There are also stories of remodelers rolling up their sleeves to help, starting with Nardo and Gottlieb, who set up a website through Truevolv to connect employees affected by the Renovo shutdown with home improvement and remodeling companies looking to hire.

In New England, homeowners left mid-project by NEWPRO Home Solutions found an unlikely lifeline in Long Home, a family-owned remodeler that launched “Project Rebuild” to help affected customers finish abandoned projects. “They just got burned, so we want to build trust,” said Katie DePaola, Long Home’s director of people and communications. “If a customer calls us and their bathroom is mid-demolition, we’ll assess the situation for free and see how we can help pick up where it was left.”

Long Home has honored deposits up to $3,000 for qualifying homeowners and hired several former NEWPRO employees. It’s not a scalable solution—and it isn’t meant to be. It’s a reminder of how reputational damage from a financial collapse radiates outward, affecting competitors who had nothing to do with the original deal.

Consumer finance will change

Beyond the employees and the customers is a hidden casualty. Jim Campbell, a 30-year veteran in consumer financing at Wells Fargo, says the least-discussed casualty so far in the collapse of Renovo Home Partners is the network of lenders that funded the remodeling projects before any work was completed. “Most of these home improvement companies are using consumer financing to help them sell jobs,” Campbell said. “The top ones are selling upwards of 90% of their jobs” through consumer lenders. Large players like Renovo routinely use “advance funding,” in which finance companies disburse funds to the contractor before the project is finished—and sometimes before it starts.

When Renovo shut its doors, the funded balances remained on customers’ accounts. “Now the customers are being billed for that, and those consumer lenders are out of this money essentially. When the consumer says, ‘I didn’t receive any services,’ they have to credit it back.” Wells Fargo’s practice, he said, is to automatically refund those affected, but not all lenders do the same. Some will “try to stick it to the customers to reduce their losses.” Either way, someone on the lending side is absorbing a real loss on jobs that will never be installed.

Mike Petrakis, CEO of PowerPay, said Renovo’s fallout is familiar. “I’ve watched this happen in other industries,” he said. “There was a pool contractor with dozens of holes in the ground when they went under,” Petrakis ended up securing all the subcontractors and completing every project, so homeowners weren’t left with open pits. “The customers didn’t deserve to pay for a company’s bad cash flow,” he said. His point: when a large contractor fails mid-project, lenders, subs, and customers all get caught in the blast zone.

When financed jobs are advance-funded, today’s sales are often used to cover yesterday’s obligations. The model works—until it doesn’t. Both Petrakis and Campbell characterize it the same way: “Advance funding is a drug,” says Petrakis, “once you use it to cover yesterday’s job with tomorrow’s revenue, it’s almost impossible to get off.” When a company relies on those early draws to cover overhead and past jobs, it becomes very hard to step off the treadmill. “It’s a line of credit for the dealer that they’re drawing on,” Campbell said. “If the faucet gets shut off on the new jobs, then how do you pay for the old jobs?”

Uneven impact across the market

The broader implication for the industry is still unfolding. Campbell expects tighter underwriting, lower advance percentages, and greater scrutiny of dealer creditworthiness—changes that could hit small and mid-sized remodelers hardest. He’s already seeing a widening split between companies serving affluent markets with premium products and those working in middle- and lower-income segments with lower-priced offerings. “The companies that are dealing with affluent customers and selling higher-end products are rocking and rolling,” he said. “They haven’t lost a beat.”

By contrast, companies serving blue-collar markets are “really struggling”—not just with financing, but with basic demand and ticket size. “Where they used to go in and sell a whole house full of windows, they’re only selling the one window that needs to be replaced,” Campbell said. Lead flow, close rates, and upsell opportunities are under pressure in those markets, while customers are leaning harder on credit cards for everyday expenses, which can drag down FICO scores and approval rates. For small and mid-sized remodelers that operate in those segments and depend heavily on advance funding, the Renovo collapse could be a double hit: tighter access to their de facto line of credit and a more fragile customer base on the demand side.

Study before you sell: not all capital is the same

The Renovo collapse has reignited debate over private equity’s role in remodeling. Private equity was seen as the holy grail of the remodeling industry not too long ago, but now it doesn’t look so wise. “Let’s assume, for the sake of argument, that the private equity paid the correct amounts and there was no debt,” posits Files, “what function does a Renovo serve, and what does it actually provide? As far as I can see, the only service they offered was a job booking service—essentially an expensive agent.”

But industry voices caution against oversimplification. Different deal structures carry different risks. “At a high level, a leveraged buyout emphasizes financial structuring,” said Philip Brenckle, CFO of West Shore Home. “A buy-and-build strategy places more emphasis on long-term operational integration.” Neither model is inherently right or wrong, Brenckle said—but aggregation alone does not create value, as Burke pointed out. “The real work is building infrastructure, operating discipline, and culture before you need them,” he said. For owners contemplating an exit, the lesson isn’t that private equity is off-limits. It’s that alignment matters—between capital structure, operating philosophy, and the realities of a labor-intensive, relationship-driven business.

“Nobody knows how to sell a business until you sell a business,” states Gottlieb matter-of-factly. It is critical to work with people who specialize in this sort of thing—someone who speaks the language. He likens it to hiring: “Just like you’re interviewing an employee, you want to interview potential buyers if you are a seller; it’s got to be a good culture fit.” Don’t get “googly-eyed” and start talking too much and sharing your P&Ls too soon.

As a former one of those eager investment bankers, Files said his co-workers would go through a few questions before closing deals that may be instructive to business owners being courted by buyers:

• We all know what can go right, what will go wrong?

• Can the current crop of managers and leaders do the job?

• What if the projections are optimistic? What if they are pessimistic? And can we fire the person who made the projections if they are off by N%?

• The Monkey and the Pedestal model: Is the company driven by a sunk cost fallacy?

• How can the company grow, how can it shrink, and can it pivot?

• Who is the competition? Can we buy, block, or kneecap them?

A failure worth understanding

Despite the fallout, Renovo may ultimately strengthen the industry’s private-equity landscape. Multiple people we spoke with think it will be a case study for investors to look at. It’s a blip on the radar of a much larger market, as Owens pointed out, but it offers a solid lesson. Investors may learn what not to do and why. Coupled with the creditor takeover of SageHome, there’s evidence that the Renovo situation is part of a larger pattern of roll-ups built on unrealistic expectations. Nardo concurs: “There are others that are going to fail because I know other groups that came in during COVID that are rolled up that are having similar problems.”

The damage—to employees, customers, lenders, and local reputations—is real and ongoing. But so is the opportunity to learn from it. Remodeling is resilient. The work itself hasn’t changed. What has changed is the industry’s understanding of how quickly financial engineering can overwhelm operational reality—and how expensive that lesson can be when it finally arrives.

Leveraged Buyout vs. Buy to Build: What They Are—and How They Work

Not all private equity-backed acquisitions operate the same way, even when they appear similar from the outside. Philip Brenckle, CFO of West Shore Home, draws a clear distinction between two approaches that carry very different implications for operating companies.

Leveraged Buy Out assigns the cost of the company as new debt to the company

“At a high level, a leveraged buyout typically emphasizes financial structuring — using debt to acquire businesses and relying on performance and efficiency gains to support that leverage,” Brenckle said.

In that model, the acquired company is expected to generate enough cash flow—or operational improvement—to service the debt placed on it. When conditions are favorable, leverage can magnify returns. When conditions change, that same leverage can quickly become a constraint.

Buy-to-Build looks longer term

A buy-to-build strategy, by contrast, shifts the emphasis from financial engineering to operations. “A buy-and-build strategy, in theory, places more emphasis on long-term operational integration,” Brenckle said. That includes “investing in management infrastructure, systems, culture, and organic growth, so the platform can scale sustainably over time through both acquisition and other means.”

Neither one is right or wrong

Brenckle is careful not to frame the distinction as moral or ideological. “Neither model is inherently right or wrong,” he said. “But they carry very different risk profiles.” Where those differences tend to surface most clearly is in service businesses that rely heavily on people and local execution. “In labor-intensive, customer-facing businesses, the ability to absorb change and integrate operations often becomes more important than financial leverage alone,” Brenckle said.

In other words, the question is not simply how a deal is financed, but what the business is being asked to do after the transaction closes—and whether its operations are built to support that expectation over time.

About the Author

Daniel Morrison

Editorial Director

Daniel Morrison is the editorial director of ProTradeCraft, Professional Remodeler, and Construction Pro Academy.

Jay Schneider

Senior Editor

Jay Schneider is the Senior Editor for Pro Remodeler. He can be reached at [email protected].