Getting Out: Remodelers Need an Exit Strategy

The Exit Gap: Most Remodelers Aren't Ready to Leave

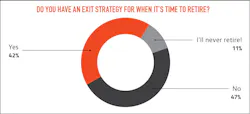

Ask remodeling business owners about their exit strategy and the camps are divided: 47% said they have no exit strategy while 42% said they have a solid plan in place.

Those results come from a survey that Pro Remodeler conducted this spring asking owners about their plans for when they eventually leave their companies. The survey reveals a wide gap between when owners plan to retire and how prepared they actually are to do so.

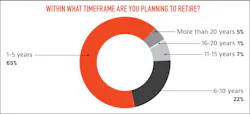

That split isn’t necessary great news since a well-executed exit strategy takes three to five years of dedicated preparation. With 65% of respondents saying they hope to retire within the next five years, and nearly 80% reporting to be in the age range of 60 to 70-plus, those who haven’t started planning are already behind. For the 22% who said they plan to retire within 6-10 years, there’s no time better than the present to start getting things in order.

What Owners Are Planning to Do

Among those who have explored or settled on an exit strategy, selling to employees is the most common path at 33%. Selling to family members and simply closing shop tied at 23% each. Selling to an outside buyer came in last at 21%.

Interestingly, 70% of respondents said they do not currently have family members working at their company. As for the pool of outside buyers, it’s a shallow one. Most private equity and strategic buyers target companies above a certain revenue threshold, so with 93% of respondents reporting annual revenues below $10 million, they aren’t attractive targets. Further, private equity is a less likely option following the Renovo collapse earlier this year.

The Challenges Keeping Owners From Acting

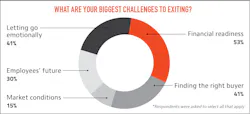

Financial readiness is the top barrier to exiting, cited by 53% of respondents. Finding the right buyer and letting go emotionally tied at 41%. Remodeling companies are built around the founder's relationships and decision-making, so a successor has to be capable of sustaining what was built and ideally expanding on it. And the emotional consideration is real because the business can be the identity for a lot of owners—especially when 88% said they have been in business for more than 20 years.

Only 20% of respondents have had their business professionally valued. That means 80% of owners don't actually know what their company is worth and the number they're counting on for retirement may not match what the market or a potential buyer is able or willing to pay.

When it comes to feeling prepared for their eventual exit, only 16% said they are very prepared and 45% feel somewhat prepared. That means a significant 40% said they are not very prepared or not prepared at all. There are a lot of remodelers not prepared for their hoped-for retirement within the next five years.

Post-Retirement Plans

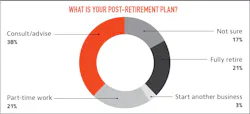

Most owners don't plan to stop working entirely. Only 21% said they'll fully retire and another 21% said they expect to stay on part-time while 38% plan to consult or advise. These results suggests that for most remodelers, exit means a shift in role rather than a clean break.

What Every Owner Needs to Consider Before They Exit

David Lupberger spent 25 years as a remodeling contractor in Washington, D.C., before founding Contractor Transition Strategies in Denver. He focuses on helping remodelers plan their exit from their company, and he’s found that they often don’t start early enough, are unsure how to start, and haven't thought about what happens afterward. His starting point with every clients involves the same three questions:

- When do you want to leave? Be specific because a vague intention to exit “in a few years” is not a plan and a proper exit strategy typically takes three to five years to execute. Think of it in terms of the design-build process, Lupberger says. “We're going to design an exit, and then we're going to implement the exit.”

- Is there an asset gap? This is the difference between what owners are currently earning and what they’ll need to live on post-retirement. If there's a gap, the transition window is also a value-building window, and you need to know that before you start, not after.

- Who is your successor? If you don't have a clear answer, this is where the work begins. Lupberger suggests using a vesting process of 24 to 36 months for any potential successor—family member or employee—with regular evaluation checkpoints. The goal is to determine whether someone has the entrepreneurial drive to actually run a company, not just the willingness to own one. More often than not, he says, the drive isn't there because most people want security rather than the risk that comes with ownership. Better to find that out during a structured vesting period than after the transfer.

Know Your Selling Options

Moving on from that starting point, Lupberger walks owners through three possible exit strategies.

A sale to a strategic third-party buyer can produce a fast, clean exit, but culture is the biggest risk. What a buyer is willing to pay and what an owner believes the company is worth rarely match, and a strategic buyer may not share the same commitment to employees that the owner spent years building.

Selling to a key employee or family member is the preferred route if the right person or people are in place, partly because it allows for financing flexibility. If a successor doesn't have the capital to buy the business outright but they are qualified, Lupberger suggests a structure along the lines of a phantom stock: a promise to transfer ownership at a future date, tied to performance benchmarks and funded by putting a portion of the successor's bonuses into escrow over time until they've effectively purchased the business.

The third path is an employee-owned cooperative, which is different from an ESOP. An employee stock ownership plan is generally built for companies doing $10 to $12 million or more annually, because setting one up means creating a trust and incurring extensive legal costs. A cooperative works for smaller companies. In a co-op, it's one person, one share, one vote, and profit distribution is based on patronage, meaning hours worked. New hires typically join the co-op as a condition of employment, with a modest entry fee paid down over time through payroll.

Can Your Business Be Sold?

Lupberger is direct about the fact that not every remodeling business is sellable. For example, if a company is netting around $50,000 a year after owner's compensation, and the owner is still working 50 hours a week, the company likely isn’t an attractive option, and buyers—employees or otherwise—are unlikely to be interested. The fix is building real profitability and a business that runs on systems rather than the owner's personal effort. “You should always be building a business that is not dependent on you,” Lupberger says. “If it's not dependent on you, it's transferable.”

Time is Not on Your Side

Forbes has projected that 2.5 million businesses will be for sale by 2030 as baby boomers retire. The estimate is that 80% of those businesses will never sell, because the owner is the business and never did the work of separating from it. Lupberger compares the lack of planning to procrastinating on a will. “There's no urgency until there is,” he says of how most owners approach the issue.

One more thing most owners skip entirely: A business continuity plan. Lupberger says most of his clients come to him without a plan in place, and that leaves most small businesses exposed. Consider, if you're five years from your exit and something happens to you, what does your company do? Who is the banker, the attorney, the insurance agent? Are those relationships and passwords documented somewhere that your team can easily access?

Have a Post-Retirement Plan

The Exit Planning Institute reported that around 75% of business owners experience “profound regret” within 12 months of selling their company, which does not surprise Lupberger. “Can you let go?” is a question he asks all of his clients. Owners are turning over everything they’ve worked on and lived with for the past 20 to 25 years or more, so they need to figure out what’s going to replacing that. “Where does that passion go to next?” is what every business owner needs to consider before making their exit, says Lupberger.

What a Lawyer Wants You to Know Before Buying or Selling

Attorney D.S. Berenson has spent more than 30 years focused on the remodeling sector. Here's what he says everyone should understand when buying or selling a company in the home improvement space.

- Seek legal counsel from someone who understands the industry. “You hear people saying I'm not bringing a lawyer in because they're just going to kill the deal. But if you have good counsel, it can go a long way to making sure that everybody feels they're protected,” Berenson says.

- Understand the industry’s unique due diligence concerns. Again, this is why it’s important to retain a lawyer who understands the home improvement space. The biggest liability issues: customer contract compliance, telemarketing violations, lead paint rules, deceptive advertising practices, and independent contractor classification. These items aren't on a standard due diligence checklist.

- Get an NDA in place before you share anything. You need legal protection the moment you start disclosing financials, customer data, or operational details to a potential buyer. Standard NDAs in the industry run two years, but Berenson suggests pushing for a minimum of five years.

- Then disclose everything. Sellers are being sued after closing, not always for dishonesty, but for failing to document how they handled certain regulatory issues. "When in doubt, disclose it out," Berenson says. Having clear documentation that covers every sensitive area of operations is the best protection a seller has.

- Understand how your assets are classified. In remodeling, you're largely selling goodwill, meaning the customer database, the brand, and the lead generation structure, among other things. Goodwill is taxed at the capital gains rate, which is lower than ordinary income. Many buyers have paid more in taxes than necessary because their documents didn't explicitly attribute the sale price to goodwill. Get an accounting opinion before you sign.

- Know that a contractor's license does not transfer with a sale because it’s not an asset that can be purchased. It has to be approved through the appropriate contractor board, a process that can take weeks or months. Berenson says he’s been contacted by frustrated buyers after deals closed. “The new owner can’t run a single job while the board sorts it out. The license is frozen. They can't run their leads. They can't finish the work in progress. They can't do the installs.”

The Hardest Exit is the One Complicated by Family

Alan Hendy has spent the better part of a decade navigating the intersection of family, ownership, and leadership at Neil's Design Remodel. Here's what he learned.

Alan Hendy will be the first to tell you that running a family business and transitioning out of one are entirely different things. He's spent years learning that distinction at Neil's Design Remodel, a design-build firm founded by his father in Cincinnati more than 50 years ago.

Hendy is the youngest of three brothers who ran the company through its growth years, helping it realize $12 to $15 million in annual revenue. However, for a long time, everyone was selling and nobody was effectively in charge, Hendy says. He affectionately refers to the situation as a “three-headed monster.”

From Three Brothers to One Leader

The moment of clarity came in 2012, during a business education program at Aileron, a small-business think tank outside Dayton, Ohio. On the drive home, his brothers looked at Alan and told him he needed to run the place. "You like the people stuff," they said, so Alan took over management.

In 2015, the family took a step that Hendy considers one of the most important things they did: they wrote a family charter. The document was developed with the help of a professional facilitator and defines three overlapping circles—family, ownership, and business—and laid out clear rules for each. “People have to make sure their business values match up with their family values,” Hendy says. “We don't all sit around and talk about family values, but at work we frame them and hang them on the wall.”

The charter addresses who is eligible for ownership, how new family members enter the company, what perks and compensation look like, and how decisions get made when family and business interests pull in different directions.

When The Heir Apparent Isn't

A difficult chapter in the company’s leadership transition happened more recently and has delayed Alan’s exit from the company. The individual who was positioned as the company’s next leader wasn’t the right fit, so they were bought out in March. Hendy says the situation was painful, but he has no regrets about how it was handled and he knows it was the right call. He notes that having a written charter doesn't prevent conflict, but it gives everyone a shared document to point to and one that was agreed to before any conflict arises.

Advice for Other Remodeling Company Owners

Hendy's advice to owners navigating family succession starts with one instruction: listen to your team, not just your family. "I can think of three very large companies in this industry right now that are absolutely going to face this," he says. "When I sit down with the owners, none of it comes up. Five minutes later, I'm having a drink with someone on their team and that's all they're talking about."

More advice: Give an heir apparent a long runway with real accountability, not just a title and an assumption. And build an advisory board with people who have no stake in the outcome. “The better my management team got, the less important the family last name became,” he says.

The Third Time’s the Charm

John Happel's path to a worker cooperative took two failed attempts and a near-disaster along the way.

John Happel didn't arrive at his exit strategy easily. The founder of design-build firm H&H Builders in Denver tried twice before getting it right, and one of those attempts nearly cost him everything.

The First Attempts at an Exit

His first attempt was a salesperson hired with the explicit intention that he'd eventually buy the business. That deal fell apart within six months. The second attempt nearly cost him everything. Happel brought on someone who would take over, and as Happel transitioned to working fewer hours he stopped monitoring the books as closely as he should have.

The individual had stopped paying vendors, and before Happel discovered the problem, the company was saddled with more than $100,000 in debt. “I have since found out that this situation isn’t uncommon,” Happel says. “Multiple owners I’ve talked with have had a similar experience or heard of a similar experience.”

That was 2019, and Happel has since rebuilt the business, recapitalized it, and came back roughly twice the size it had been.

A Different Kind of Buyer

Going into a third attempt, Happel was understandably cautious. Working with a consultant, Happel was introduced to the concept of a worker cooperative. It turns out Colorado is the leading state for them, with favorable laws and tax credits. In Happel's case, the credit covered more than $50,000 in setup costs.

Conventional advice when selling a business is not to tell employees until the deal is closing, but when setting up a co-op, the employees are the buyers and the transition is open and collaborative. There is a financial logic to it, too. In a traditional sale, owners often leave 30 to 40% of their equity on the table in the form of a seller's note, waiting years to be paid out in full. “That's a long time to stay attached to something you've already let go,” Happel says.

H&H is now structured as a worker cooperative, with six founding members out of 10 employees. Each member who joins receives one share and an equal claim to profits. There is an initial buy-in of a few thousand dollars, with a full share price payable over five years through payroll deductions, bonuses, or profit distributions. The company’s sale was structured as a note to Happel that will be paid out to him from company profits over five years.

The one surprise: No outside lender would finance the deal, so Happel had to carry the note himself. “That's a big drawback,” he says. “You have to maintain involvement longer than if you'd sold it traditionally.” His phased exit runs at least four more years.

Figuring Out How to Leave, and What to Leave With

David and Renata Callahan have been in the remodeling business since 1983. Getting out is proving to be its own project.

David Callahan will be 75 this year. He still likes unlocking the door at his remodeling firm Callahan & Peters in Glenview, Ill., every morning. But the years pile up, and his wife Renata, a company co-owner, is ready for them to retire.

Their succession plan is taking shape gradually. Their nephew David Peters has been with the company since 1998, and it was always understood he would eventually take over. The company’s designer, Michelle Chircop has been with the company for 11 year and remains another key player alongside Peters. The Callahan’s daughter Renee, who had previously worked at the company, may also become a part of the transition plan.

So, while the target is clear, it’s been harder to achieve their exit.

“I'm so busy working in the business, that I'm having a hard time working on getting out of it,” David says.

The Callahan’s retained a consultant in the fall of 2024, and they realized the checklist of things they need to complete was a big one. They admit to having felt a little overwhelmed at first but it also helped ramp things up. “It forced us to address issues, but it's actually an intriguing and fun process,” David says. “The trick is finding the time.”

Among their tasks: transition the responsibilities associated with accounting, payroll, and bill paying; rewriting job descriptions; and scrutinizing the company’s org chart looking for gaps. Renata's target is to be out by March 2027, but David expects to stay on part-time, perhaps handling sales and being “of counsel,” as he describes it.

On the question of price: it’s not their primary concern, noting they can retire without proceeds from the business. The structure may involve residuals tied to company performance or a formula for getting income out of it over time, but they said the baseline plan is closer to a transfer than a sale. “If we walk away with no money, they've still got a company that's producing for them and their families,” David says. “That's what matters most to us.”

He adds: “I'm not going to stress. I want to hand them something that works well for them, and I want them to be successful and happy.”

One piece of advice David wants to pass on: Don't try to make decisions for the people who'll be running the business once you exit. Initially, he considered opening the ownership opportunity to the full staff, and his consultant advised against it. David recalls being told to let the new owners make that decision and to avoid complicating the process.

What to know about ESOPs before setting one up

An employee stock ownership plan has real advantages, but the structure can be more complex than people realize. Here's what an owner who is involved in one (and who wishes to remain anonymous) wants other remodelers to understand before they commit to an ESOP.

- ESOPs work best for companies with annual revenues of at least $10 million. The legal and accounting costs of creating and maintaining an ESOP trust, including annual valuations, ongoing tax filings, and independent audits once a plan exceeds 120 participants, generally make them impractical for smaller companies. For those businesses, an employee cooperative achieves similar ownership goals with less overhead.

- The payout timeline is a significant consideration. When a departing employee's shares are paid out over an extended period and the share price rises during that time, the company ends up paying former employees at current higher valuations for work done years ago. Before setting up the plan, think carefully about how you want to handle the timeline and whether converting shares to cash at the time of departure makes more sense for your situation.

- CEO incentives need to be addressed separately. In a 100% ESOP, shares are allocated based on each employee's salary as a percentage of total payroll. In a company with many employees earning similar wages, a CEO might end up holding only 2% to 3% of the company, which is far less than in virtually any other ownership structure. That's a meaningful disincentive for attracting strong executive leadership. Hybrid models, where a CEO holds a personal equity stake alongside the ESOP, are becoming increasingly common. Stock appreciation rights and deferred compensation structures are other tools worth exploring.

- The cultural upside is real. Employees who own a piece of what they're building tend to behave differently. They stay longer, take more ownership of their work, and are more sensitive to whether the company is running profitably. For many owners, that cultural shift is the primary reason to pursue an ESOP plan.

A Buyer’s Perspective

Not every exit involves selling to a family member or employee. In some instances, an outside party may already be looking for you. West Shore Home, a national home improvement company that acquires regional remodeling businesses, shared what they look for when evaluating a potential acquisition and what owners can expect if they pursue that path.

What Do You Look For, What's The Curb Appeal?

When we evaluate a potential acquisition, the “curb appeal” is largely centered around the fit. We look for businesses with strong local reputations, great teams in place, owners who care deeply about the businesses, and meaningful overlap with our core services: residential bath remodeling, windows, doors, and flooring. Additionally, we are especially interested in businesses that have capable leaders already in place who can help support a smooth transition and continue growing the business.

What’s on the inspection checklist?

Our due diligence process is designed to be efficient, focused, and non-invasive. We want to understand the fundamentals of the business (financial performance, facilities, organizational structure, leadership, culture, and overall operational fit) without disrupting the day-to-day operations while we do it.

What’s the transition like?

We have a dedicated integration team that helps make the process as smooth as possible for the existing management team, employees, and customers. Our goal is to bring a business into the West Shore Home operating model (including our branding, technology, operations, marketing, and customer experience platform) so that the business can continue to grow in a consistent and sustainable way.

About the Author

Jay Schneider

Senior Editor

Jay Schneider is the Senior Editor for Pro Remodeler. He can be reached at [email protected].